The AI infrastructure buildout is now one of the largest capital deployment cycles in modern history. Alphabet, Amazon, Meta and Microsoft are expected to spend roughly $650 billion on AI-related infrastructure in 2026. China’s hyperscalers, provincial governments and state-backed platforms are spending tens of billions more.

The headline story is compute abundance. The operating reality is messier.

China is carrying the cost of capacity planned around policy targets, cheap land and assumed demand. The United States has stronger demand visibility, but power, equipment and permitting are now slowing the physical buildout.

Both markets are still building. Both are also showing the limits of capital-led infrastructure planning.

For operators, capital allocators and policymakers in India, the UAE, Saudi Arabia, Singapore and Malaysia, this creates a narrow strategic window. The geographies that build with discipline over the next 24 months can absorb capital that no longer fits cleanly into either China or the United States. The geographies that copy the mistakes will inherit the same stranded-capital problem, just with newer logos.

China's problem: capacity without fit

China's installed datacenter capacity reached roughly 32 GW at the end of 2025 and is projected to reach 40 GW by the end of 2026, according to Rystad Energy. AI and HPC facilities account for around 39% of that base today, with that share expected to rise toward 48% by 2030.

The scale is impressive. The portfolio quality is uneven.

China's Eastern Data Western Computing programme pushed datacenter investment into western provinces such as Inner Mongolia, Gansu, Ningxia, Guizhou and Sichuan. These regions offered land and power. They did not always offer demand proximity, chip access, workload fit or utilisation.

Reported utilisation across newer western capacity has often sat around 20% to 30%. Other reporting, citing MIT Technology Review and Chinese sources, has described a much larger share of newly built compute as effectively unused. Regulators have started imposing utilisation thresholds and purchase-contract requirements on new projects, according to reporting on China's response to the overbuild.

The project count matters. MIT Technology Review reporting, as summarised by TechRadar, points to more than 500 AI datacenter projects announced in China and at least 150 completed by the end of 2024. If up to 80% of new computing resources are idle, that does not mean 120 buildings are literally empty. It does mean that the output of roughly 100-plus project-equivalents is missing from the AI economy.

Another way to size the problem is by power. If China reaches 40 GW of installed datacenter capacity by the end of 2026 and 15 GW to 20 GW is stranded, under-filled or running materially below economic utilisation, the capital tied to low-yield capacity is enormous. At $5 million to $10 million per MW for older and mixed-spec facilities, that implies roughly $75 billion to $200 billion of gross capex exposed to weak returns. The truly unrecoverable slice is smaller, because some shells can be repurposed or re-tenanted, but even a 25% impairment on that pool is a $20 billion to $50 billion balance-sheet problem.

| China estimate | Public datapoint | AISIGINT interpretation | |

|---|---|---|---|

| Projects announced | 500+ | Policy-driven buildout created too many parallel projects | |

| Projects completed by end-2024 | 150+ | Large enough base for utilisation problems to matter now | |

| New compute idle or weakly used | up to 80% in local reporting | Equivalent to 100+ project-equivalents of missing output | |

| Installed capacity by end-2026 | ~40 GW | 15-20 GW plausibly underutilised or economically impaired | |

| Capex tied to weak-return capacity | AISIGINT estimate | ~$75B-$200B gross exposure; ~$20B-$50B impairment risk |

Weak Chinese AI demand and restricted access to Nvidia chips both matter. They still do not fully explain the overhang.

The deeper issue is structural mismatch.

First, many shells were designed for older cloud and general compute workloads. Modern AI infrastructure is moving into a different density class: AI deployments already run at 40 kW per rack and above, while next-generation rack-scale systems such as Nvidia's GB200 NVL72 are liquid-cooled designs built around dense GPU domains. Some deployment guides put GB200-class racks around 120 kW. A facility built for yesterday's rack density can become economically obsolete before it fills.

Second, demand was assumed rather than contracted. Many western-region projects were built on the expectation that state-owned enterprises and government agencies would consume large volumes of compute. That demand did not arrive at projected scale.

Third, political incentives rewarded announcement volume. Gigawatt-scale project announcements create visible progress. Capacity-demand fit is less visible until after the capital is spent.

Fourth, chip access and build planning were not sufficiently coupled. The US has since moved to a case-by-case licensing regime for advanced chips such as the Nvidia H200 and AMD MI325X into China, with security conditions attached under the US Bureau of Industry and Security framework. Chinese import approval and demand have remained politically complex.

China still has significant AI demand, especially around large platforms. Those buyers are more likely to want high-density campuses near talent, customers and network hubs than mis-specified capacity in distant provinces.

America's problem: demand without energisation

The American constraint has a different shape.

Demand is real. Capital is available. Site selection is generally closer to customers, talent and network ecosystems. The issue is that physical infrastructure cannot move at software speed.

Roughly 12 GW of US datacenter capacity has been expected to come online in 2026, but industry reporting based on Bloomberg and Sightline Climate data suggests that close to half of planned US builds may be delayed or cancelled. Transformer lead times, switchgear availability, interconnection queues and local permitting are now gating AI deployment.

Sightline Climate's tracking, as reported across the industry, puts the 2026 US pipeline at roughly 12 GW to 16 GW across about 140 projects, with only around 5 GW under active construction. That leaves 7 GW to 11 GW in the risk zone for 2026 delivery. If 30% to 50% of projects slip, that is roughly 40 to 70 project-equivalents that do not become usable AI capacity on the expected timetable.

Transformer delivery timelines are a useful proxy for the problem. Reporting on the US market suggests high-power transformer delivery has moved from roughly 24 to 30 months before 2020 to as long as five years today in some cases, while other 2026 market trackers put large transformer lead times in the 60 to 120 week or multi-year range depending on voltage class and specification.

A multibillion-dollar campus can be delayed by electrical infrastructure representing a small fraction of total project cost. The expensive assets are GPUs, servers, networking and buildings. The schedule risk often sits in transformers, breakers, substations, grid studies and approvals.

The United States did not spend the last two decades building the industrial base required for a rapid doubling of datacenter load. That gap is now meeting a hyperscaler capex cycle that assumes much faster delivery.

This is bigger than Nvidia revenue timing. It is a risk to the entire 2026-2028 AI infrastructure cycle. GPU orders tied to delayed campuses do not disappear, but they slip into future calendars that are already congested.

Why this hits the token economy

The practical consequence is not only fewer buildings. It is lower token-production capacity.

The current AI economy is increasingly a token economy. Model companies, cloud platforms, enterprise copilots, agentic workflows and sovereign AI programmes all depend on a growing supply of usable tokens: tokens for training, tokens for evaluation, tokens for synthetic data, tokens for inference, tokens for agents calling other agents. Demand is not measured only in users or seats. It is measured in how many useful tokens can be produced, served and paid for.

Datacenter delays therefore become token supply constraints. A delayed AI campus does not just defer rent. It defers GPU deployment, model training runs, inference capacity, enterprise rollouts and the feedback loops that improve future models.

Here is a simple H100-equivalent framing. It is not a universal benchmark, because token output depends on model size, batch size, precision, utilisation, memory bandwidth and serving stack. But it is useful for sizing the order of magnitude.

| Assumption | Conservative case | Higher-throughput case | |

|---|---|---|---|

| H100-equivalent GPUs per 1 MW IT load | 600 | 800 | |

| Useful output tokens per second per GPU | 100 | 400 | |

| Token-production capacity per 1 MW IT load | ~5B tokens/day | ~28B tokens/day |

On that basis, 7 GW to 11 GW of US 2026 capacity at risk is not just a construction delay. It is roughly 35 trillion to 300 trillion tokens per day of delayed gross production potential, depending on workload mix and serving efficiency. China's 15 GW to 20 GW of underutilised or economically impaired capacity represents another 75 trillion to 550 trillion tokens per day of theoretical output that is either not available, not in the right place, not attached to the right chips, or not commercially useful.

Those numbers should not be read as forecast revenue. They are a capacity lens. A training cluster does not produce saleable inference tokens every second. A frontier model and a small enterprise model do not have the same throughput. Utilisation is never 100%. Still, the direction is clear: when gigawatts slip or sit idle, the token economy loses output headroom.

| Capacity problem | GW affected | Token-production implication | |

|---|---|---|---|

| US 2026 projects at risk of delay | 7-11 GW | ~35T-300T tokens/day delayed gross potential | |

| China underutilised or impaired capacity | 15-20 GW | ~75T-550T tokens/day trapped or misallocated potential | |

| Combined China + US drag | 22-31 GW | ~110T-850T tokens/day of gross token headroom not arriving cleanly |

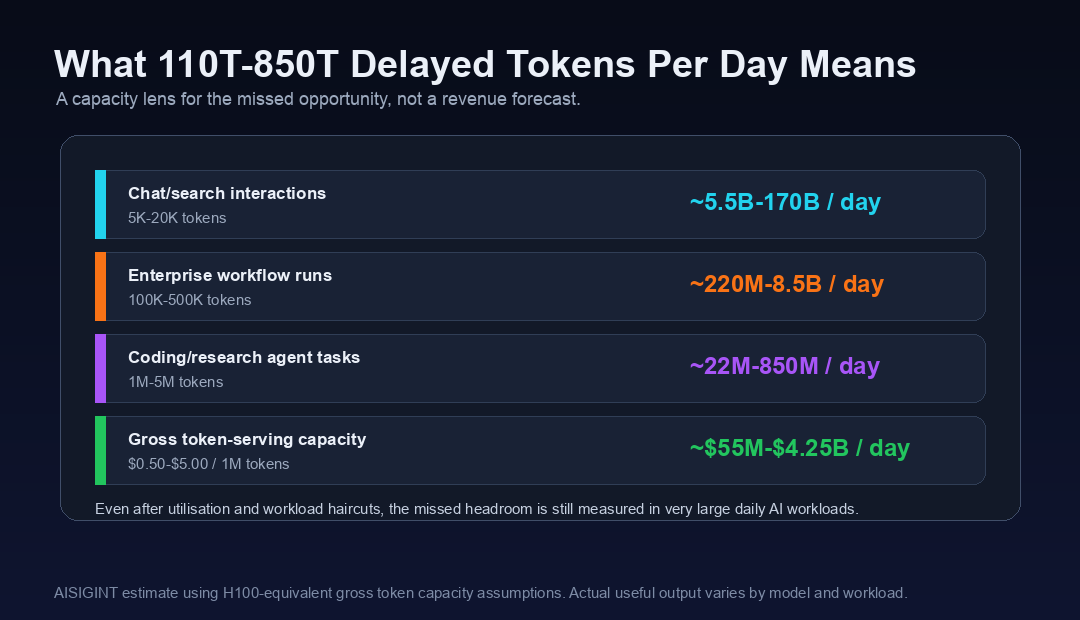

To make that less abstract, assume a simple chatbot or search-style interaction consumes 5,000 to 20,000 total tokens across prompt, context, reasoning and answer. Assume a serious enterprise workflow consumes 100,000 to 500,000 tokens once retrieval, tool calls, document context and validation are included. Assume a coding or research agent consumes 1 million to 5 million tokens for a meaningful multi-step task. The combined China-US drag then maps into very large units of missed AI work:

| Unit of AI work | Token assumption | What 110T-850T delayed tokens/day could support | |

|---|---|---|---|

| Chatbot/search-style interactions | 5K-20K tokens each | ~5.5B-170B interactions/day | |

| Enterprise document or workflow runs | 100K-500K tokens each | ~220M-8.5B workflows/day | |

| Coding/research agent tasks | 1M-5M tokens each | ~22M-850M agent tasks/day |

This is gross capacity, not demand that automatically monetises. The useful number after utilisation, workload mix, latency requirements and reserved training capacity would be much lower. Even at 10% effective conversion, however, the missed headroom is still measured in hundreds of millions of daily AI interactions or tens of millions of heavier agent tasks.

There is also a dollar lens. Current API pricing across frontier and mid-tier models is commonly quoted per million tokens, with separate input and output rates on OpenAI and Anthropic. If delayed token capacity would have cleared the market at a blended $0.50 to $5.00 per million tokens, the combined China-US drag represents roughly $55 million to $4.25 billion per day of gross token-serving capacity. That is not a revenue forecast. It is a way to understand the scale of the production bottleneck.

This is why the datacenter mismatch matters for future AI demand. If token supply is constrained, three things happen at once. Prices stay higher for longer. Enterprise adoption slows because inference capacity is not available at the price and latency buyers need. Model development gets more concentrated among the few players with guaranteed access to energised, high-density capacity.

The bottleneck then feeds back into demand. Some demand disappears because products cannot launch. Some demand is deferred because token prices are too high. Some demand moves geographically because buyers follow available capacity. The next wave of AI growth will therefore be shaped not just by model quality, but by where usable token-production capacity actually comes online.

The bifurcation

China is working through misallocated capacity. America is working through delivery bottlenecks.

That bifurcation matters because the next layer of AI infrastructure will not be built only in the two largest markets. India, the Middle East and Southeast Asia are now credible destinations for AI datacenter capital, especially where they combine demand growth, political support, grid access, land availability and operator depth.

But the opportunity is conditional.

India has roughly 1.3 GW to 1.5 GW of datacenter capacity today, with 2030 projections varying widely. Some estimates point to around 4 GW by 2030, while others see the market reaching 4-5 GW or materially higher depending on AI demand, cloud adoption and power availability.

If the next wave is built as headline capacity without rack-density discipline, power-path validation, demand mapping and evidence-backed site selection, India risks creating its own version of idle shells.

If the next wave is built with American-style optimism around grid interconnection, transformer procurement and permitting timelines, India risks a different failure: funded projects that cannot energise on time.

The window is real, but the margin for error is narrow.

What disciplined buildout looks like

Disciplined AI datacenter development has four non-negotiable properties.

1. Rack density must match the chip generation. A 2026 site that cannot support 40 kW per rack is already constrained. A 2027 AI-heavy build needs a credible path toward much higher densities, direct-to-chip liquid cooling, stronger floor loading and power distribution designed for AI clusters. Nvidia is already pushing an 800 VDC architecture for future AI factories, with partners working on the power chain needed for high-density AI racks.

2. Location must be selected for demand fit, not just cheap power. Power cost matters, but customer proximity, fibre, cloud ecosystem presence, regulatory access, enterprise sales motion, construction depth and operational talent all matter. A low-cost site that cannot attract the right workload becomes expensive very quickly.

3. Grid, equipment and permits must lead the shell. The American lesson is simple: the least glamorous parts of a datacenter project can delay the most expensive parts. Interconnection, transformer procurement, substation path, land conversion, environmental clearances and local acceptance need to be validated before capital is locked into concrete.

4. Chip supply and commissioning milestones must be tied together. A gigawatt-scale AI campus only becomes useful when accelerator availability, delivery timing and power-on sequencing line up. Shell-first planning without chip-path confidence creates optionality on paper and stranded capital in practice.

These are practical checks against failures already visible in China and the United States.

The opportunity

The next decade of AI infrastructure value will concentrate in geographies that get the next 24 months right.

India, the UAE, Saudi Arabia, Singapore and Malaysia do not need to outspend the United States or China. They need to out-execute them at the project level: better site selection, better evidence, better grid realism, better permit sequencing, better demand matching.

That requires a different diligence standard.

Static PDFs, high-level market commentary and informal grid comfort are no longer enough. AI-era capital needs execution intelligence: which projects can energise, which sites are mis-specified, which permits are real, which power paths are credible, and which risks are moving after the investment committee approves the deal.

The buildout is global. The capital is mobile. The mistakes are already visible.

Discipline is the difference between becoming the next AI infrastructure hub and becoming the next overbuild story.

How AISIGINT helps

AISIGINT works with infrastructure funds, operators, lenders and advisors evaluating AI datacenter pipelines across India, Southeast Asia and the Middle East.

If you are screening sites, preparing an IC memo, reviewing a JV opportunity or pressure-testing a live pipeline, get in touch. We can run evidence-backed diligence on a single site or a portfolio of candidate locations.

We work on an NDA basis and understand that site coordinates, power pathways, tenant discussions and acquisition processes are sensitive.

*Data sources: Bridgewater estimate via Investing.com, Rystad Energy China datacenter outlook, Tom's Hardware on China utilisation, TechRadar on China overbuild, US BIS advanced chip licensing policy, Tom's Hardware on US 2026 delays, TechSpot summary of Sightline Climate 2026 pipeline data, Build Inc on substation procurement, pv magazine USA on transformer lead times, India Infrastructure data centre market report, CARE Ratings India datacenter capacity note, Economic Times Energy on India 2030 capacity, Nvidia 800 VDC architecture.*